By Jim Snelson May 26, 2026

Reading time: 7 minutes

If you’ve just taken over as club treasurer — or you’ve been doing it for years but never quite trusted that the numbers line up — bank reconciliation is the single most important habit you can build. It’s also one of the most misunderstood. This guide explains what a bank reconciliation actually is, why it matters for clubs and societies specifically, and how to do one properly every month.

What is a bank reconciliation?

A bank reconciliation is simply a check that the money your records say you have matches the money your bank says you have. Your treasurer’s records (whether in a spreadsheet, a notebook, or accounting software) are one version of the truth. Your bank statement is another. When they agree, you know your records are accurate. When they don’t, something has gone wrong and you need to find it before it compounds.

The differences usually come from one of four places:

- Timing differences — a cheque you wrote hasn’t been cashed yet, or a payment in transit hasn’t cleared

- Bank-side transactions you didn’t know about — interest, fees, direct debits, standing orders

- Data entry errors — a £45.00 entered as £54.00, or a duplicate

- Missing transactions — a member’s payment that hit the bank but never made it into your records

A good reconciliation finds all four. A bad one papers over them and lets the gap grow.

Why bank reconciliation matters more for clubs than for businesses

Most accounting guides are written for businesses, but clubs and societies have unique pressures that make reconciliation even more important:

You answer to a committee, not a boss. Members ask awkward questions at the AGM. “Why does the bank balance not match the report?” is a question you do not want to answer on your feet.

You hand over to a successor. Unlike a business finance team, club treasurer roles change every few years. A clean reconciliation history means your successor inherits a working system, not a forensic project.

You may need to satisfy a governing body or auditor. CASCs, charities, and clubs affiliated to sports governing bodies often face external scrutiny. Reconciled accounts are the foundation of any audit, independent examination, or grant application.

You handle other people’s money. Members trust you with subs, donations, and event takings. Reconciliation is how you prove — to yourself first — that nothing has gone astray.

How often should a club treasurer reconcile?

Monthly, in line with your bank statement. That’s the gold standard, and it’s also the easiest. The longer you leave it, the more transactions pile up and the harder errors are to find. A monthly rhythm of an hour or so beats an annual marathon of a full day every time.

If your club has multiple bank accounts — current, deposit, PayPal, Stripe, a debit card account — reconcile each one separately, every month.

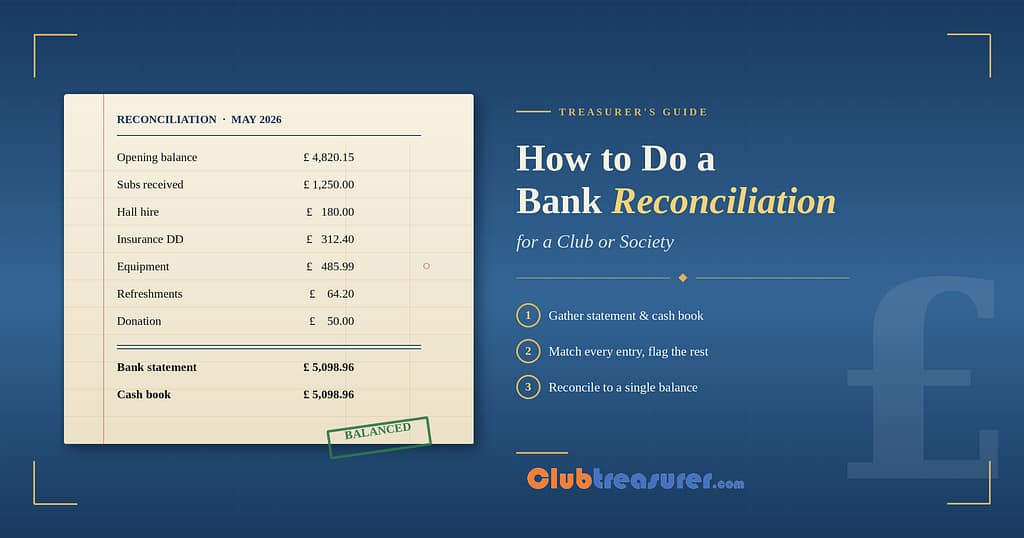

The step-by-step process

Here’s the process that works whether you’re using a spreadsheet, paper ledger, or dedicated software:

1. Gather your materials. You need the bank statement covering the period and your transaction records for the same period.

2. Check the opening balance. The opening balance on this month’s statement should match the closing balance from last month’s reconciled records. If it doesn’t, stop — something has changed in a prior period and you need to find it before going further.

3. Tick off the matches. Go through your records and the statement line by line. For every transaction that appears on both, mark it as reconciled. Watch for: matching amounts on different dates (timing difference, fine), matching dates with different amounts (error, investigate), and transactions on one side but not the other (missing entry, investigate).

4. Investigate the unmatched items. Anything left unticked falls into two camps. Items on your records but not on the statement are usually timing differences (uncashed cheques, pending transfers) — note them and they’ll appear next month. Items on the statement but not in your records need to be added: bank fees, interest, member payments you didn’t know had landed.

5. Confirm the closing balance. Once everything is matched or accounted for, your records’ closing balance should equal the bank statement’s closing balance. If it does, the reconciliation is complete. If it doesn’t, the difference equals the value of items still in dispute — work through them until the gap closes.

6. Lock it down. Once reconciled, those transactions should not be edited. This is the discipline that protects your audit trail. If you find an error in a reconciled transaction later, you should unreconcile, fix, and re-reconcile — never just edit silently.

Common pitfalls

Forcing the numbers. If your reconciliation is £2.37 out and you can’t find it, the temptation is to add a “balancing entry.” Don’t. That £2.37 is real money somewhere, and the discipline of finding it is what builds reliable records. (The one exception: tiny historical errors inherited from a previous treasurer, which sometimes warrant a formal opening-balance adjustment with committee approval.)

Reconciling against the wrong date. Bank statements run on the bank’s calendar, not yours. Make sure the period you’re reconciling matches the statement period exactly, or you’ll chase phantom differences.

Treating PayPal or Stripe like a bank account afterthought. Online payment processors are bank accounts for reconciliation purposes. They have fees, timing delays, and chargebacks — they need the same monthly treatment as your current account.

Letting it slip for “just one month.” One missed month becomes three. Three becomes a year. A year becomes a panic in the week before the AGM. Put it in your calendar as a recurring task the day after your statement arrives.

A treasurer’s monthly reconciliation checklist

- Statement(s) downloaded for the period

- Opening balance agrees with last month’s closing

- Every statement line matched against records

- Bank fees and interest added to records

- Unpresented cheques noted and carried forward

- Closing balance agrees

- Reconciliation saved or signed off

- Reconciled transactions locked from edit

Making it easier

You can absolutely do all of this in a spreadsheet, and many clubs do. But once you have more than one account, recurring memberships, or a committee who wants to see reports without being emailed a new file each month, dedicated software starts to pay for itself in time alone.

Clubtreasurer is a UK-based accounting platform built specifically for clubs, societies, and not-for-profits. It handles monthly bank reconciliation in a few clicks, automatically locks reconciled transactions to protect your audit trail, and supports multiple accounts, funds, and cost codes designed around how clubs actually operate — not businesses. If you’d like to see how it works, you can start a free trial or browse our bank reconciliation walkthrough in the user guide.

Whatever tool you choose, the principle is the same: reconcile monthly, find every difference, lock down what’s done. Do that and your accounts will be in better shape than 90% of clubs in the country — and your AGM will be a lot less stressful.